Orca Gold: Preliminary Economic Assessment of Block 14 Strong Economics at US$1,200/oz

Orca Gold: Preliminary Economic Assessment of Block 14 Strong Economics at US$1,200/oz

VANCOUVER, BRITISH COLUMBIA--(Marketwired - July 26, 2016) - Orca Gold Inc. (TSX VENTURE:ORG) ("Orca" or the "Company") is pleased to announce the results of a Preliminary Economic Assessment ("PEA") prepared pursuant to National Instrument 43-101 (NI 43-101) on the Company's 70% owned Block 14 Project in the Republic of the Sudan (Figure 1).

The PEA, prepared by SGS Time Mining of South Africa, shows a strong economic project at a gold price of US$ 1,200/oz, with in-pit indicated resources of 1.22Moz and inferred resources of 0.14Moz and a pre-tax NPV7% of US$ 156 million and an IRR of 25% and an after-tax NPV7% of US$ 128 million and an IRR of 22%.

The PEA is based on contract mining with ore treated at Galat Sufar South (GSS) through a 1.8Mtpa standard carbon-in-leach ("CIL") processing plant. Process water will be supplied from a bore-field 55km north of GSS where the Company has discovered water in a Nubian Sandstone Aquifer system (see News Release dated July 5, 2016).

Highlights of the Block 14 PEA on a 100% Basis

Using a gold price of US$ 1,100/oz for mine design, and US$ 1,200/oz for economic analysis, highlights of the PEA include:

- Pre-tax NPV7% of US$ 156 million and an IRR of 25%;

- After-tax NPV7% of US$ 128 million and an IRR of 22%;

- In-pit mineral resources comprising 25.07Mt grading 1.52g/t for 1.22Moz in the indicated category and 2.80Mt grading 1.51g/t for 0.14Moz inferred resources.

- 1,053,302 ounces of gold produced from indicated resources and 117,034 ounces produced from inferred resources over life of mine ("LOM");

- Mine life of 16 years with average annual LOM production of 73,000 ounces of gold;

- Average annual production in years 1-5 of 82,400 ounces of gold;

- Average gold recoveries of 86%;

- Cash costs of US$ 778/oz for LOM;

- All-in Cash costs of US$ 805/oz for LOM;

- Initial capital costs of US$ 123 million (including a 19% contingency);

- Sustaining capital costs of US$ 31 million; and

- Payback period of approximately 4 years, after-tax, from commencement of production.

Sensitivities:

| Gold Price (US$/oz) | 1,100 | 1,150 | 1,200 | 1,250 | 1,300 |

| Pre-tax NPV7% (US$ millions) | 91 | 123 | 156 | 189 | 222 |

| After-tax NPV7% (US$ millions) | 72 | 100 | 128 | 156 | 184 |

| Pre-tax IRR (%) | 18 | 22 | 25 | 29 | 32 |

| After-tax IRR (%) | 16 | 19 | 22 | 25 | 28 |

A summary of the key results from the PEA is provided below in Appendix A with further detail on PEA inputs by discipline in Appendix B. SGS Time Mining ("SGS") was engaged by Orca Gold to produce an independent PEA for the Block 14 Gold Project. A technical report following the guidelines of the Canadian Securities Administrators' National Instrument 43-101 will be filed on Sedar and on the Company website within 45 days.

Opportunities to Enhance Value

The PEA has demonstrated a strong project with several opportunities for improvement. Accordingly, the Board of Orca has approved the decision to complete a Pre-Feasibility Study ("PFS") of the Block 14 project focused on optimizing the Project towards a development decision in 2017.

The PFS will focus on the following material opportunities:

Metallurgy

Test work during the PEA has indicated that gold deportment is very closely related to sulphides (+90% of which are pyrite). Preliminary testing has shown positive results from the use of flash flotation within the grinding circuit with subsequent regrinding of the concentrate. This has the potential to increase overall LOM recoveries by 2-3%.

Tailings

The use of a tailings filter press for dry stack tailings disposal enabling the recovery of a larger proportion of the water, which will reduce the volume of water pumped from the aquifer will also be investigated as part of the study.

Throughput

The PEA set processing throughput at 1.8Mtpa pending confirmation of water production rates from the HA8 bore field, north of Block 14. The PFS will look at the economics of increasing throughput and reducing the mine life from 16 years to 12-15 years.

Geotechnical

Overall pit slopes used in the PEA are conservative at 35° in oxide and transition and 47° in fresh rock. The development of the pits is very sensitive to the slope angles, particularly in fresh rock. The PFS will include a geotechnical drilling programme to determine whether, and to what extent, pit slopes can be steepened.

Confirmation of Water Supply

As part of the PFS, 5 large diameter production bore holes will be drilled at the H8 Aquifer in order to fully test the production rates, and to determine if mining throughput can be increased beyond 1.8Mtpa.

Reserve Definition

10% of the in-pit resources are currently in the inferred category, a short RC drill programme will be carried out to upgrade these into indicated resources and to provide coverage in several areas where the pits show the potential to go deeper. The PFS will declare project reserves for the first time.

Exploration

Given the large exploration permit area (3,750km2), prospective geological setting and clear gold endowment as indicated by the large numbers of artisanal miners, Block 14 continues to demonstrate significant potential for resource expansion. Exploration will continue during the PFS evaluation.

Timing

The PFS is scheduled for completion by the end of Q1 2017.

Hugh Stuart, President and CEO, commented, "With the completion of the PEA we now have an initial look at the strong economic potential of the Block 14 project. The grade of the deposit, low strip ratio, metallurgical response, and relatively low capital and operating costs are all strong factors which create value. However, we believe that there is significant potential upside through optimisation of various aspects of the project. Accordingly, Orca's Board of Directors has approved the immediate commencement of a PFS, targeted for completion by the end of Q1 2017. With the delivery of a positive PFS we look forward to working with the Government and people of Sudan towards the development of a commercial gold mine."

PEA Contributors

- SGS Time Mining Ltd, Lead Author, Overall Project design.

- Deswik Europe Ltd, Mine Design and Scheduling.

- SRK Consulting UK Ltd, Geotechnical Review.

- MPR Geological Consultants, Mineral Resource Estimate.

- SGS Mineral Services, Metallurgical Test work.

- GCS Water and Environmental Consultants, Hydrogeology.

- Mineesia, Environmental and Social Consultant.

- Propipe Pipeline and Projects, Water Pipeline Design

- Kevin Ross, Consultant, Overall PEA Oversight.

- Mike Hallewell, Consultant, Metallurgical Oversight.

The reader is advised that the PEA summarized in this press release is intended to provide only an initial, high-level review of the project potential and design options. The PEA mine plan and economic model include the use of Inferred resources. Inferred resources are considered to be too speculative to be used in an economic analysis except as allowed for by Canadian Securities Administrators' National Instrument 43-101 (NI 43-101) in PEA studies. There is no guarantee that Inferred resources can be converted to Indicated or Measured Resources.

Qualified Persons

The technical contents of this release have been approved by Hugh Stuart, BSc, MSc, a Qualified Person pursuant to NI-43101. Mr. Stuart is President and CEO of the Company and a Chartered Geologist and Fellow of the Geological Society of London. Mr. Stuart has reviewed and validated that the information contained in this release is consistent with that provided by the QP's responsible for the PEA.

About Orca

Orca Gold Inc. is a Canadian resource company focused on exploration opportunities in Africa, where it is currently focused on its 70% owned Block 14 project in the Republic of the Sudan. The Company has an experienced board of directors and management team and a strong balance sheet, with a treasury of approximately CAD 14.7 million at June 30, 2016.

On behalf of the Board of Directors:

Hugh Stuart, President, CEO and Director

Cautionary Statement Regarding Forward-Looking Information

This press release contains "forward-looking information" within the meaning of applicable Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as "anticipate", "believe", "plan", "expect", "intend", "estimate", "forecast", "project", "budget", "schedule", "may", "will", "could", "might", "should" or variations of such words or similar words or expressions or statements that certain events "may" or "will" occur. Forward-looking statements in this press release include, but are not limited to, statements relating to indicates and inferred mineral resources, the potential to expand the resource targets in the Main and East Zones, the plans of the Company to conduct preliminary metallurgical test work and increase its ownership in Block 14 and the future potential of GSS to become a commercial mining operation, including exploration activities. Forward-looking information is based on reasonable assumptions that have been made by the Company as at the date of such information and is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking information, including but not limited to: risks associated with mineral exploration and development; metal and mineral prices; availability of capital; accuracy of the Company's projections and estimates; interest and exchange rates; competition; stock price fluctuations; availability of drilling equipment and access; actual results of current exploration activities; government regulation; local political instability or unrest, local economic instability; global economic developments; environmental risks; insurance risks; capital expenditures; operating or technical difficulties in connection with development activities; personnel relations; the speculative nature of strategic metal exploration and development including the risks of diminishing quantities of grades of reserves; contests over title to properties; and changes in project parameters as plans continue to be refined. Forward-looking statements are based on assumptions management believes to be reasonable, including but not limited to the price of gold; the demand for gold; the ability to carry on exploration and development activities; the timely receipt of any required approvals; the ability to obtain qualified personnel, equipment and services in a timely and cost-efficient manner; the ability to operate in a safe, efficient and effective manner; the expected timing, costs, and results of a PEA; the expected burn rate; the regulatory framework regarding environmental matters, and such other assumptions and factors as set out herein.

Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. The Company does not undertake any obligation to update forward-looking information if circumstances or management's estimates, assumptions or opinions should change, except as required by applicable law. Accordingly, readers should not place undue reliance on forward-looking information contained herein.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

APPENDIX A

PEA Summary at a Gold Price of US $1,200/oz*

| Indicated Resources Mined (tonnes) | 25,071,067 |

| Average Grade of Indicated Resources (Au g/t) | 1.52 |

| Inferred Resources Mined (tonnes) | 2,801,240 |

| Average Grade of Inferred Resources (Au g/t) | 1.51 |

| Total Waste (tonnes) | 58,704,152 |

| Strip Ratio (Waste:Ore) | 2.1 |

| Gold Contained in Indicated resources (oz) | 1,225,204 |

| Gold Contained in Inferred resources (oz) | 135,994 |

| Total Gold Produced from Indicated resources (oz) | 1,053,302 |

| Total Gold Produced from Inferred resources (oz) | 117,034 |

| Average Gold Recovery (%) | 86% |

| Average Annual Gold Production (oz) | 73,146 |

| Total Initial Capital Cost (including 19% Contingency) | 122,580,134 |

| Total Sustaining Capital (Including 19% Contingency) | 31,290,040 |

| Total Life of Mine Capital (Including 19% Contingency) | 153,870,174 |

| Total LOM Operating Cash Flow (US$) | 448,015,841 |

| Total LOM Pre-tax Cash Flow (US$) | 462,677,678 |

| Average Annual LOM Pre-Tax Cash Flow (US$) | 28,917,374 |

| LOM Taxes (US$) | 45,952,177 |

| Total LOM After-Tax Cash Flow (US$) | 416,725,801 |

| Average Annual LOM After-Tax Cash Flow (US$) | 26,045,363 |

| Discount Rate | 7% |

| Pre-Tax NPV (US$ millions) | 156,343,241 |

| Pre-Tax IRR | 25.3% |

| Pre-Tax Payback (years) | 3.3 |

| After-Tax NPV (US$ millions) | 128,221,307 |

| After-Tax IRR | 22.1% |

| After-Tax Payback (years) | 3.7 |

| Cash Cost (US$/oz) | 778 |

| All-in Cash Costs Including Sustaining Capex (US$/oz) | |

| Mining | 235 |

| Processing and G&A | 454 |

| Refining | 5 |

| Royalties | 84 |

| Sustaining | 27 |

| All-in Cash and Sustaining Cost (US$/oz) | 805 |

*The reader is advised that a PEA is preliminary in nature and there is no certainty that the PEA results can, or will, be realized. Mineral resources do not have demonstrated economic viability, and therefore do not constitute mineral reserves. The reader is also advised that the PEA results contained in this news release are only to provide an initial economic assessment of the project.

To view Figure 1: Block 14 Location, please visit the following link: http://media3.marketwire.com/docs/Fig1Block14Orca.jpg

{kind=link}

APPENDIX B

PEA DETAILS

Mineral Resources

Updated Mineral Resource estimates were carried out by independent consultant Nic Johnson of MPR Geological Consultants of Perth, Western Australia using Multiple Indicator Kriging (MIK), and are shown below at various cut off grades.

| Galat Sufar South | ||||||

| Cut off | Indicated | Inferred | ||||

| Au g/t | Mt | Au g/t | Au koz | Mt | Au g/t | Au koz |

| 0.2 | 109.0 | 0.79 | 2,769 | 52 | 0.7 | 1,170 |

| 0.4 | 72.6 | 1.04 | 2,428 | 30 | 1.0 | 965 |

| 0.5 | 60.7 | 1.16 | 2,264 | 25 | 1.1 | 884 |

| 0.6 | 50.9 | 1.27 | 2,078 | 20 | 1.2 | 772 |

| 0.8 | 36.3 | 1.51 | 1,762 | 14 | 1.4 | 630 |

| 1.0 | 26.3 | 1.74 | 1,471 | 10 | 1.7 | 547 |

| 1.2 | 19.3 | 1.97 | 1,222 | 7 | 1.9 | 428 |

| 1.5 | 12.3 | 2.33 | 921 | 4 | 2.3 | 296 |

| Wadi Doum | ||||||

| Cut off | Indicated | Inferred | ||||

| Au g/t | Mt | Au g/t | Au koz | Mt | Au g/t | Au koz |

| 0.2 | 3.31 | 1.48 | 158 | 12.5 | 0.6 | 241 |

| 0.4 | 2.42 | 1.91 | 149 | 5.6 | 1.0 | 180 |

| 0.5 | 2.15 | 2.10 | 145 | 4.2 | 1.2 | 162 |

| 0.6 | 1.94 | 2.27 | 142 | 3.3 | 1.3 | 138 |

| 0.8 | 1.60 | 2.60 | 134 | 2.1 | 1.7 | 115 |

| 1.0 | 1.36 | 2.91 | 127 | 1.4 | 2.1 | 95 |

| 1.2 | 1.17 | 3.19 | 120 | 1.0 | 2.4 | 77 |

| 1.5 | 0.96 | 3.59 | 111 | 0.7 | 3.0 | 68 |

| Combined | ||||||

| Cut off | Indicated | Inferred | ||||

| Au g/t | Mt | Au g/t | Au koz | Mt | Au g/t | Au koz |

| 0.2 | 112 | 0.81 | 2,926 | 64.5 | 0.7 | 1,411 |

| 0.4 | 75.0 | 1.07 | 2,576 | 35.6 | 1.0 | 1,145 |

| 0.5 | 62.9 | 1.19 | 2,409 | 29.2 | 1.1 | 1,046 |

| 0.6 | 52.8 | 1.31 | 2,220 | 23.3 | 1.2 | 910 |

| 0.8 | 37.9 | 1.56 | 1,896 | 16.1 | 1.4 | 745 |

| 1.0 | 27.7 | 1.80 | 1,599 | 11.4 | 1.7 | 641 |

| 1.2 | 20.5 | 2.04 | 1,342 | 8.0 | 2.0 | 505 |

| 1.5 | 13.3 | 2.42 | 1,032 | 4.7 | 2.4 | 363 |

The Mineral Resource has been estimated using the results of 73,579 metres of drilling (5,310m of diamond drilling and 68,269m of reverse circulation drilling, including 250m and 10,062m respectively at Wadi Doum) completed between November 2012 and December 2015.

Mining

The Mining section of the study has been completed by Deswik UK. Both GSS and Wadi Doum are amenable to development as open pit (OP) mines as all mineralization commences at surface with limited pre-strip. Mining of the deposit is planned to produce a total of 25.07 Mt of CIL feed from Indicated Resources and 2.80Mt of feed from Inferred Resources and 58.7 Mt of waste (2.1:1 overall strip ratio) over a 16-year project production life with no capitalized pre-stripping.

Mine planning for Block 14 was conducted using DESWIK software. Pit slopes range from 35° to 47° as derived from a preliminary geotechnical assessment completed by SRK Consulting (UK) Ltd.

Pit optimizations were carried out using a gold price of US$1,100/oz. and a series of optimized shells generated for each area and preliminary pit design undertaken based on a feed rate of 1.8Mtpa.

Cut off grades (Au g/t) were estimated as follows:

| Material | GSS Main Zone | GSS East Zone | Wadi Doum |

| Oxide | 0.59 | 0.59 | 0.87 |

| Transitional | 0.63 | 0.63 | 0.93 |

| Fresh | 0.73 | 0.79 | 1.05 |

Contract open pit mining costs were derived from first principles based on equipment required and include pit and dump operations, road maintenance, mine supervision and technical services cost.

The average open pit operating cost per tonne mined is shown below:

| Function | US$/t |

| Drill and Blast | 0.81 |

| Loading | 0.27 |

| Haulage | 0.57 |

| Wadi Doum Ore Transport | 0.20 |

| Ancillary | 0.49 |

| Mine Administration | 0.83 |

| Total | 3.17 |

In compliance with NI43-101, the PEA study is based on Indicated and Inferred Mineral Resources. The table below shows the breakdown of material by resource type within the pit designs:

| Deposit | Indicated Resources | Inferred Resources | % Indicated | ||||

| Mt | Au g/t | Koz | Mt | Au g/t | Koz | ||

| Galat Sufar South | 23.77 | 1.44 | 1,101 | 2.10 | 1.27 | 85.8 | 92% |

| Wadi Doum | 1.30 | 2.90 | 121 | 0.70 | 2.21 | 49.7 | 65% |

| Total | 25.07 | 1.52 | 1,221 | 2.80 | 1.51 | 136 | 90% |

| Note: Numbers may not add up due to rounding |

Processing

Based on the results of metallurgical test work by SGS Mineral Services in the UK and South Africa, SGS Time Mining have defined a process flowsheet which includes three stage crushing (crush size -8mm) followed by ball milling (to -75um) and standard carbon in leach.

The process flowsheet is based on a processing rate of 1.80 million dry tonnes per year.

The estimates for ultimate gold recovery were based on the results of laboratory tests conducted by SGS Mineral Services in the UK and South Africa. A summary of the ultimate recoveries used in the study is summarized below:

| Deposit | Facies | Au Recovery % |

| Galat Sufar South | Oxide | 92 |

| Transition | 87 | |

| Fresh | 80 | |

| Wadi Doum | Oxide | 83 |

| Transition | 83 | |

| Fresh | 83 |

Process Cost Summary

The table below details the Process costs used in the study which are inclusive of general and administrative costs.

| Deposit | Material Type | Pcost US$/t |

| Galat Sufar South | Main Oxide | 17.83 |

| Main Trans | 17.92 | |

| Main Fresh | 19.13 | |

| East Oxide | 17.83 | |

| East Trans | 17.83 | |

| East Fresh | 20.71 | |

| Wadi Doum | Oxide | 20.12 |

| Trans | 20.12 | |

| Fresh | 20.12 |

Power will be generated on site using a combination of Heavy Fuel Oil (HFO) and diesel generators. Costs of $US 0.45/l and $0.65/l respectively have been used in determining the process costs.

Capital Cost Summary

A breakdown of the capital cost estimates is shown below:

| Item | US$ Million |

| General / Plant Wide | 3.55 |

| Tailings Storage Facility Area | 5.60 |

| Primary Crushing | 6.44 |

| Secondary & Tertiary Crushing | 3.92 |

| Material Handling | 0.39 |

| Coarse Material Stockpile | 0.27 |

| Fine Material Stockpile | 1.42 |

| Primary Mill Circuit | 8.46 |

| Reagents | 0.49 |

| CIL | 9.71 |

| Elution | 2.57 |

| Electro-winning | 0.71 |

| Gold Room | 1.07 |

| Dewatering | 2.31 |

| Mining & Waste Rock Area | 2.00 |

| Utilities & Services | 1.14 |

| Water Treatment & Storage | 1.39 |

| Fuel Storage | 0.43 |

| Power Generation | 13.44 |

| Water Supply | 20.12 |

| Sub-total Direct Cost | 85.43 |

| EPCM Fees / Home Office Cost @ 11.0% of Direct Cost | 11.62 |

| Field Cost @ 20.0% of Material Cost | 5.46 |

| Sub-total | 17.08 |

| Contingency @ 19.0% of Direct Cost | 20.07 |

| Total Initial Capital | 122.58 |

| Initial Capex | 122.58 |

| Deferred TSF Capex | 13.07 |

| Deferred Mining Capex | 3.00 |

| Sub-total | 138.65 |

| LOM Sustaining Capital | 15.22 |

| TOTAL LOM Capital | 153.87 |

The capital costs include the cost of a pipeline from the water supply at the HA8 bore field and an un-lined tailings storage facility. The capital costs derived by SGS Time Mining in preparation of the PEA are 40% priced on supplier quotes with the remainder based on factored estimates or benchmarking.

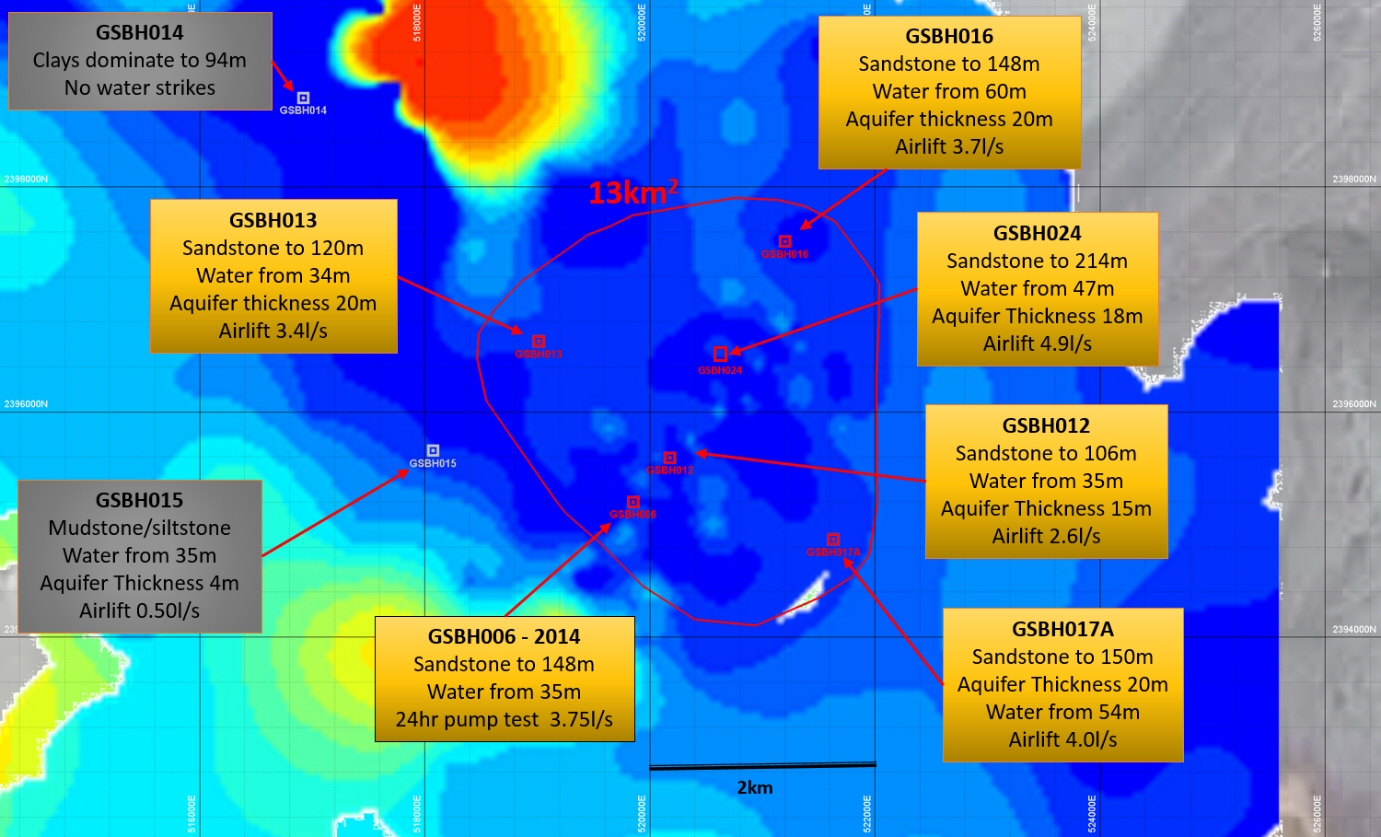

Water Supply

Process water will be supplied from the HA8 aquifer located 55km north of GSS where Orca has confirmed a water supply (figure 2 below) and the company's consultants (GCS water and Environmental Consultants) are of the opinion that, subject to final testing, the area has the potential to be able to supply the 30M m3 of water required for the project (see News Release dated July 5, 2016). Initial water pipeline design and engineering has been completed by Propipe Pipeline and Projects (Chile) and incorporated into operating and capital costs.

To view Figure 2: HA8 Aquifer, 2016 drill results, please visit the following link: http://media3.marketwire.com/docs/Fig2HA8Orca.jpg

{kind=link}

Environment

In 2014, Orca initiated comprehensive environmental baseline studies under the supervision of Mineesia, a UK consultancy with experience of remote desert projects. Terms of Reference for the Environmental Impact Assessment were submitted to the Government in 2015 as part of the Environmental Protection and Management Plan.

The site is located in a remote location, with no human settlements nearby (the closest town, Abu Hamad is 200km to the south). There are numerous artisanal and small scale mining operations in the vicinity of the Project, although these are mostly illegal and unlicensed. No other sources of industry are present in the area. There are no permanent surface watercourses within the Project area and there is limited evidence of groundwater in the crystalline basement. Soils have little to no agricultural potential. Little vegetation is present and fauna, including domestic livestock, is limited due to the scarcity of permanent water sources.

Hugh Stuart

+44 7788 487462

Please make the indicated changes including the new text: US quotes snapshot data provided by IEX. Additional price data and company information powered by Twelve Data.